Health Savings Account (HSA)

A personal account for healthcare spending, saving, and investing

Overview & Eligibility

What is a Health Savings Account?

High-deductible health plan participants use a health savings account to save tax-free earnings to pay for qualified medical expenses. It can be used to pay for current medical expenses or invested and saved for later. In short, a health savings account is a personal account for saving and investing. Employees can contribute pre-taxed earnings to their HSA to pay for current or future medical expenses such as copays, deductibles, over-the-counter medications, and prescriptions. There is no use it or lose it rule for an HSA, and the balance carries over from year to year. So, it can continue to grow, is available when needed, and can also be invested. An HSAs tax-free growth can be an added asset in planning for retirement. Only employees enrolled in an HSA-qualifying high-deductible health plan (HDHP) can enroll in an HSA, and employers receive FICA tax savings for every employee who contributes to an HSA.How can Ameriflex help?

As an industry-leading benefits administrator, the Ameriflex team can easily welcome your groups on board with personalized service and user-friendly account management. Contact our team for more information. Visit our news page to see how HSAs and HDHPs work together, or for an in-depth look at HSAs, check out our Ultimate HSA Guide.2024 Contribution Limit:

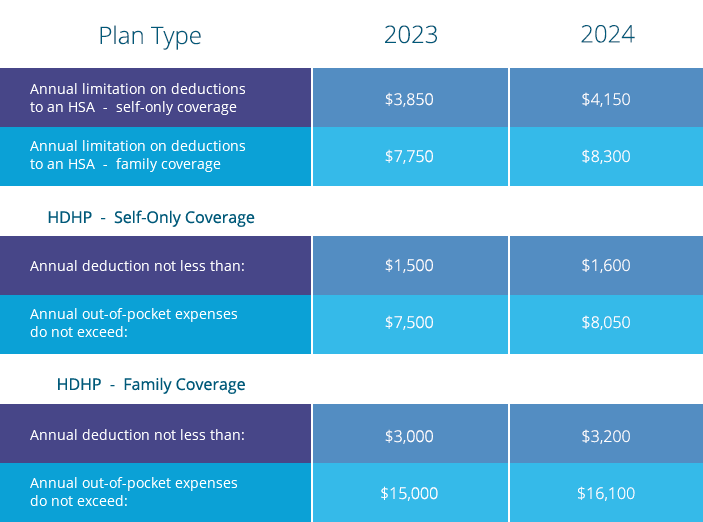

Single – $4,150

Family – $8,300

This is the maximum amount that can be contributed to an HSA each year, per the IRS.

The Value for Employees

Triple Tax Savings

Every dollar an employee contributes to an HSA lowers their taxable income, funds grow tax-free, and withdrawals for qualified expenses are tax-free.

Employee-Owned

It’s a personal savings account owned by the employee. They can keep it even if they change jobs or retire. Employees receive an Ameriflex Debit Mastercard® linked to their HSA that can be used for eligible purchases everywhere Mastercard® is accepted.

Investing & Saving

Employees can save and invest their funds with over 20+ investment options. HSA funds roll over year to year, allowing long-term growth if there are no immediate spending needs.

The Value for Employers

Cost Savings

Since contributions to HSAs are taken out pre-tax, no payroll taxes are due on the amounts employees contribute to the HSA.

Employee Engagement

Helping employees save money on their everyday medical expenses can aid in employee retention and recruitment. Employers can also make contributions to the HSA to encourage adoption.

Expert Support

The Ameriflex Client Relationship Team is eager to answer questions and provide assistance. Our Net Promoter Score (NPS) far exceeds the healthcare average.

Looking for information about your benefits?

Check out our Help Center